Millions of Americans still hold old U.S. savings bonds tucked away in safe deposit boxes, filing cabinets, or inherited from relatives. Many of those bonds are quietly reaching a critical milestone. After a certain point, they stop earning interest entirely.

Series EE and Series I savings bonds issued by the U.S. Treasury earn interest for up to 30 years. Once that period ends, the value freezes permanently. If a bond has already reached final maturity, leaving it unredeemed means the money is no longer growing.

Understanding how savings bonds work and how to redeem them before they stop earning interest can help investors avoid leaving money on the table.

Understanding Savings Bonds

Types of Savings Bonds

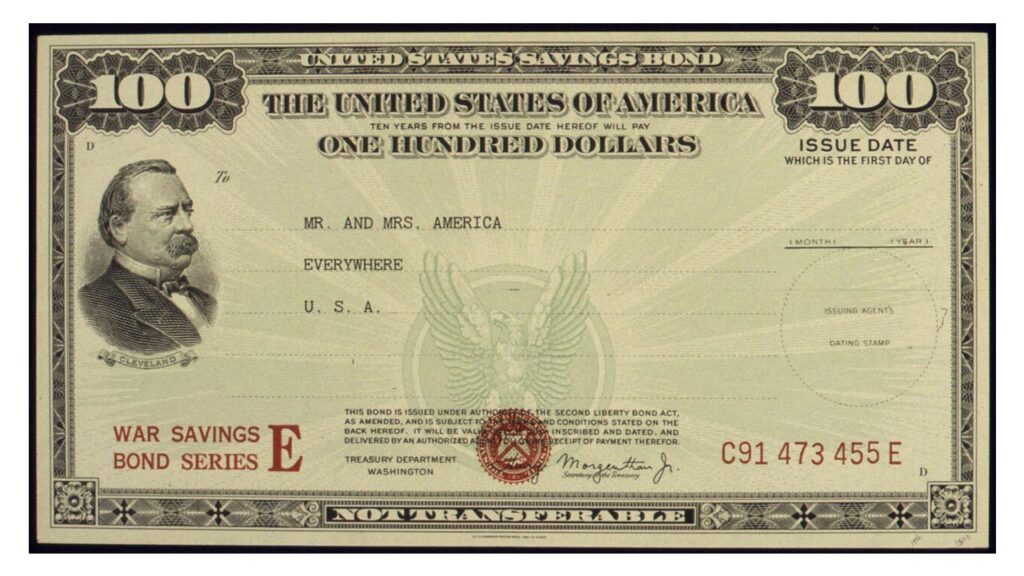

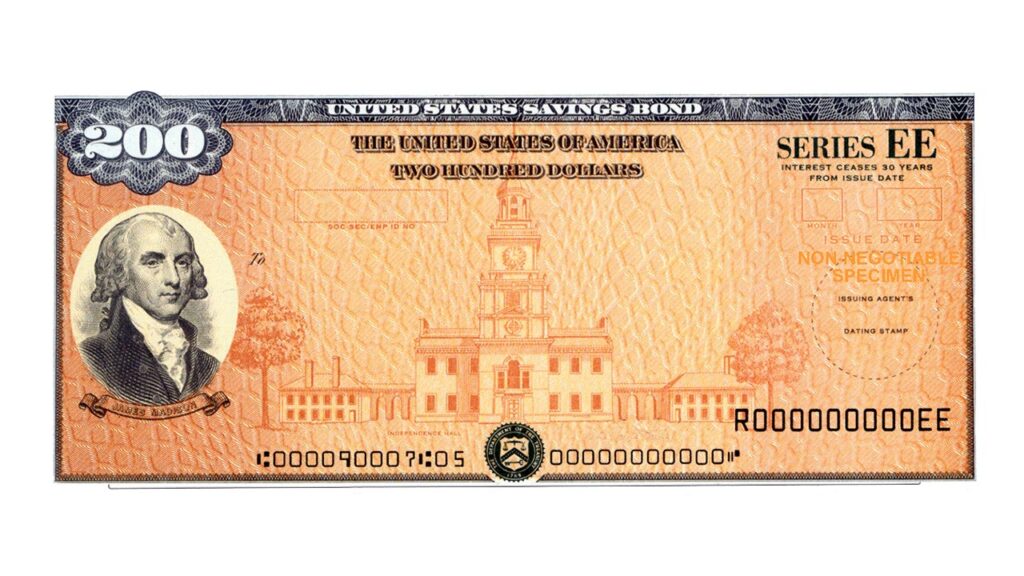

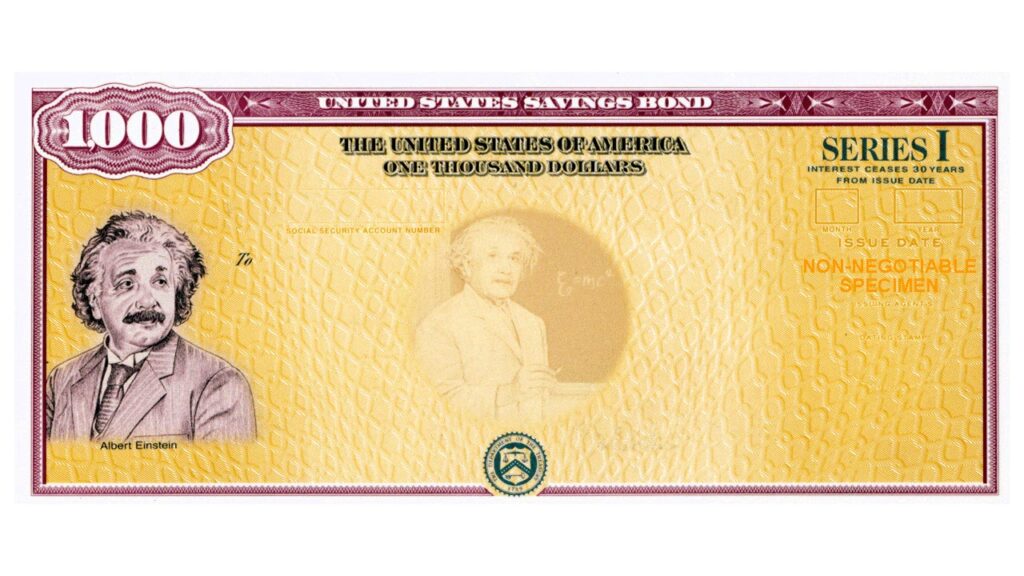

The U.S. Treasury currently issues two main types of savings bonds: Series EE and Series I. Both are considered extremely safe investments because they are backed by the full faith and credit of the U.S. government.

Series EE bonds earn a fixed interest rate, which is set when the bond is issued. The Treasury guarantees that these bonds will at least double in value if held for 20 years, making them a predictable long-term savings vehicle.

Series I bonds are designed to protect against inflation. Their rate combines a fixed component with an inflation adjustment that changes every six months based on the Consumer Price Index. This structure helps preserve purchasing power during periods of rising prices.

How Long Savings Bonds Earn Interest

While savings bonds are often described as long-term investments, they do not earn interest forever. According to the U.S. Treasury, both Series EE and Series I bonds earn interest for up to 30 years from their issue date.

Once that 30-year window passes, the bond reaches what the Treasury calls final maturity. At that point, the value stops increasing entirely. A bond that has matured will still retain its value, but it will no longer generate additional interest.

Financial experts often encourage bondholders to check older bonds to determine whether they have already reached that point. Many paper bonds issued in the 1980s and early 1990s are now reaching or have already reached final maturity.

How to Cash in Savings Bonds

Eligibility and Requirements

Savings bonds must be held for at least one year before they can be redeemed. If they are cashed in before five years, the owner forfeits the most recent three months of interest.

After five years there is no penalty for redemption. Many investors choose to wait until that point unless they need the funds earlier.

Bondholders redeeming paper bonds typically need a valid government issued ID and the physical bond certificate. Electronic bonds purchased through TreasuryDirect can be redeemed by bondholders online and transferred directly to a linked bank account.

Where to Redeem Paper Bonds

Many banks and credit unions still redeem paper savings bonds, although policies vary by institution. Customers often need to hold an account at the bank or credit union to process the redemption.

If a financial institution cannot redeem the bond, then the Treasury also allows investors to redeem paper bonds by mailing them to the Bureau of the Fiscal Service using a specific form. Detailed instructions are available through TreasuryDirect.

Taxes When Redeeming Bonds

Interest earned from savings bonds is subject to federal income tax, though it is exempt from state and local taxes. Bondholders may choose to report interest annually or defer reporting until the bond is redeemed or reaches final maturity.

In certain situations, interest may be excluded from federal taxes if the bond proceeds are used for qualified education expenses and the owner meets specific income limits. The Internal Revenue Service outlines these rules in the Education Savings Bond Program.

Maximizing the Value of Older Savings Bonds

Check Whether Your Bonds Have Matured

One of the easiest ways to determine whether a savings bond has stopped earning interest is by using the Treasury’s savings bond calculator, which is available on TreasuryDirect. By entering the bond’s series, issue date, and denomination, investors can quickly see its current value and maturity status.

This tool can be especially helpful for families who discover old bonds inherited from parents or grandparents.

Consider What to Do with the Money

Once a bond has reached final maturity, many financial planners recommend redeeming it and putting the funds to work elsewhere. Keeping the bond after it stops earning interest means the money is effectively sitting idle.

Depending on their financial goals, investors may choose to reinvest the proceeds in newer Treasury securities, high-yield savings accounts, retirement investments, or other diversified assets.

Savings bonds remain one of the safest investments available, but they are most effective when owners monitor their maturity dates and redeem them at the right time.

For many Americans, taking a few minutes to check old bonds could unlock funds that they did not realize were available.