Key Takeaways

- The coverage on a home insurance policy should be for the cost of the reconstruction of the house, not the market value.

- The fundamentals of a homeowners insurance policy include dwelling coverage, personal property coverage, liability coverage, and additional living expenses coverage.

- Special insurance coverage or endorsements are generally necessary for high-dollar items, sewer backup, earthquakes, and floods.

- Replacement Cost coverage is more financially protective than Actual Cash Value coverage since depreciation is not accounted for.

- Annual review of homeowners insurance policies can prevent homeowners from being underinsured as a result of renovations, inflation or large purchases.

Introduction

Homeowners insurance will cover the structure of a home and the personal property and financial assets that are within it following a disaster, theft or liability claim.

Home insurance coverage depends on the value of the home and its rebuilding expenses, the value of personal property, liability risks, deductibles and regional environmental dangers.

This guide details the amount of homeowners insurance coverage that you really need, how to determine coverage limits and what extra coverages might provide you with better financial protection in the long run.

Understanding Homeowners Insurance Basics

Homeowners insurance is a combination of property insurance and liability insurance. The policy safeguards the physical structure of the house, separated structures, personal property and financial risk post-covered events. The amount of protection the policy offers is defined by coverage limits, deductibles, endorsements and exclusions.

What Is Homeowners Insurance?

Its is a policy of financial protection for a covered loss of a home, its contents or liability claims. Homeowners insurance is typically a requirement of mortgage lenders since they want to have protection for the home used to secure the mortgage.

I policies usually cover the dwelling, the personal property, liability, medical payments and loss of use. There are various policies available for single-family homes, condos, rental properties, and mobile homes.

Most homeowners in the U.S. insure with a HO-3 policy, as a HO-3 policy offers coverage for the structure and coverage against named perils for personal items.

What Homeowners Insurance Covers

Typically, home insurance will cover against fire, lightning, hail, theft, vandalism, smoke damage, falling objects, windstorms, and certain water damage events. Protection for the house, separate garages, fences, sheds, furniture, electronics, appliances, and clothes.

Protection for liability is extended for legal and settlement costs in the event of injury or damage to property caused by guests. For visitors who get injured or slip near a swimming pool, liability coverage could help pay the medical expenses or legal claims. For those that are bitten by dogs in an accident, liability coverage may cover legal and medical claims.

Additional Living Expenses (ALE) coverage is for costs of temporary shelter, meals, transportation and housing when the home becomes uninhabitable due to a covered disaster.

Covered Perils

Covered perils are those events mentioned in the policy which are covered. Common coverages that give rise to a peril exclusion are:

- Fire and smoke

- Windstorms and hail

- Theft and vandalism

- Lightning strikes

- Explosions

- Falling objects

- Damage by aircraft or vehicles

- Frozen plumbing systems

A lot of policies combine Open Perils coverage for the home’s structure with Named Perils coverage on the personal property. Perils coverage only covers events on the policy. Open Perils covers against all perils except those excluded in the contract.

What Home Insurance Does Not Cover Unless You Pay More

There are a number of significant risks not covered by standard policies. Typically, policies or endorsements are necessary for flood, Earth Movement, sewer backup, landslides and earthquake damage. Flood insurance is frequently purchased separately from other coverage as a component of a National Flood Insurance Program (NFIP) policy or private insurer.

Many homeowners in coastal areas, like Southeastern Massachusetts, opt for extra flood and windstorm coverage due to increased risk from storms and seepage.

Standard policy limits may be less than the value of the items, such as high-value collectibles, jewelry, art, antiques, or high-dollar electronics. Additional coverage endorsements may be needed for home business equipment and loss of rental income.

| Coverage Type | What It Covers | Why It Matters |

|---|---|---|

| Dwelling Coverage | Structure of the home | Pays rebuilding costs after covered damage |

| Personal Property Coverage | Furniture, electronics, clothing | Replaces damaged or stolen belongings |

| Liability Coverage | Injuries and property damage claims | Protects personal finances during lawsuits |

| Additional Living Expenses (ALE) | Hotel and temporary housing costs | Helps after the home becomes uninhabitable |

| Other Structures Coverage | Detached garages, sheds, fences | Covers structures not attached to the home |

Key Factors That Affect How Much Coverage You Need

Here are some financial and structural considerations that will impact the type of coverage you should have: Coverage should be for the replacement cost rather than the market value since replacement costs can vary considerably from real estate values.

Your Home’s Rebuilding Cost

The main factor in the calculation of dwelling coverage is the home rebuilding cost. Rebuilding cost estimates encompass construction materials, labor, permits, debris removal, roofing, plumbing, electrical and contractor costs.

The cost of rebuilding a $400,000 Chicago home may be $300,000, while the reconstruction of a smaller home on the coast of Southeastern Massachusetts could cost more due to higher labor and material costs.

Dwelling coverage calculators are also used by insurance companies to estimate the replacement cost. Residents should check estimates every year as costs for rebuilding homes rise over time due to inflation and the shortage of building workers.

Your Personal Property Value

Personal property coverage is there to cover items in the home. Total value of personal property includes furniture, appliances, electronics, jewelry, kitchen equipment, clothing, tools and collectibles. Personal property replacement costs are often underestimated by many homeowners.

Having a detailed home inventory aids in the process of claims following theft or damage due to disaster and helps determine accurate values. Replacement Cost coverage covers new items at new costs – no depreciation.

Actual Cash Value (ACV) will lower payments for age and wear. Replacement Cost coverage typically offers better financial coverage.

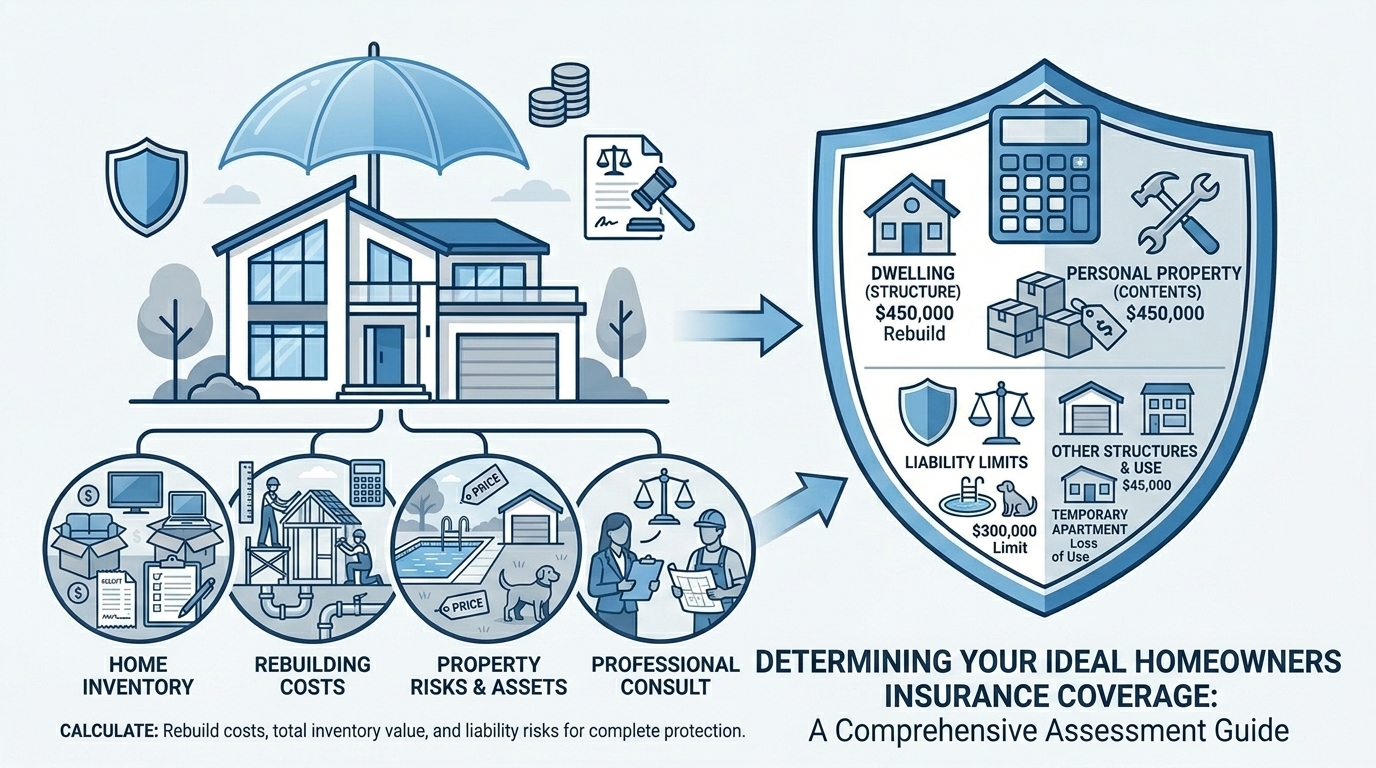

Liability Risks

During a liability lawsuit, liability coverage will protect personal finances. The liability risks increase with larger homes, pools, trampolines, dogs, rental units, and visitors. The liability coverage of most standard policies is in the range of $100,000-$500,000.

Personal umbrella policies are recommended for homeowners who hold substantial assets and are advised to have higher coverage limits. The Umbrella Insurance policy supplements homeowners and auto insurance policy limits and offers additional liability coverage.

The value of umbrella policies comes into play in major liability cases such as bodily injury or property damage claims.

Additional Living Expenses

Covered disasters force homeowners out of their homes, and Additional Living Expenses coverage covers temporary living expenses. Typically, coverage under ALE will cover laundry, meals, pet boarding, transportation and hotel expenses incurred while repairs are being made.

Homes in hurricane, hailstorm, and wildfire risk areas may need a greater ALE due to the fact that repairs following regional disasters are typically more time consuming.

Deductibles

The amount paid by the homeowner before the insurance coverage takes effect. The higher the deductible, the lower the premiums, and the more of the costs that will be covered in claims will be incurred out-of-pocket.

The $1000 deductible option means that claim costs are lower than with a $500 deductible. Some insurance companies will have a windstorm/hurricane deductible as well, depending on the percentage of your dwelling coverage.

Select deductibles based on a compromise between premium savings and having emergency financial reserves.

Special Features of Your Home

Special home characteristics add to the cost of reconstruction and to insurance requirements. Examples include:

- Custom cabinetry

- Historic architecture

- Imported flooring

- Solar panel installations

- Smart home systems

- Detached garage structures

- Underground utility lines

- Luxury kitchens

Houses in historical districts could be candidates for specialized construction materials which can be significantly more expensive for replacement.

Local Risks (e.g., Southeastern Massachusetts)

Homeowners insurance coverage and costs are highly influenced by local environmental risks. Coastal storms, coastal flooding, windstorms and winter weather hazards can be a problem for homes in Southeastern Massachusetts.

States with wildfire hazard include a price premium in their fire insurance rates. Tornado and hail damage is possible in the midwestern states. State Laws & Regulations also impact minimum coverage requirements, claims handling procedures, and premiums.

How to Determine How Much Homeowners Insurance You Need

Homeowners insurance is calculated by assessing the cost of rebuilding, valuing the personal property, assessing the liability exposure, and the risks from the environment.

Step 1: Conduct a Home Inventory

Document home inventory prior to buying or changing a policy. A home inventory lists photographs, receipts, serial numbers and replacement values of items.

Electronic spreadsheets, cell phone inventory applications and cloud storage makes recordkeeping easier. Losses Claims Process is faster due to Inventory documentation.

Insurer claims centers like GEICO Insurance Agency and Progressive typically suggest annual updates to inventories.

Step 2: Calculate Replacement Costs

Use contractor estimates, insurance calculators, real estate professionals and local builder associations to calculate replacement costs.

The following points should be considered when calculating replacement costs:

- Construction materials

- Roofing systems

- Plumbing systems

- Labor costs

- Permit fees

- Debris removal

- Temporary construction inflation

The value of a property for insurance should not be based on the old price of the property.

Step 3: Evaluate Additional Factors

Assess hazards related to pools, pets, stand-alone buildings, rental property, valuables and home business. Once substantial renovations are completed, homeowners should review coverage requirements right away since these renovations add to rebuilding costs and exposure to liability.

Step 4: Consult with Insurance Agents

Talk to insurance agents about the different structures of insurance policies, endorsements, deductibles and exclusions.

Independent agents will generally shop around among a variety of insurance companies, such as GEICO, Nationwide, Farmers Insurance, Travelers, Chubb and Progressive. Insurance professionals are able to help clarify the provisions of insurance that pertain to Open Perils, Named Perils, Replacement Cost, and Actual Cash Value.

Step 5: Leverage Builder Associations and Real Estate Agents

Builder associations and real estate agents are familiar with rebuilding trends and prices in the area. National calculators aren’t enough to get an accurate replacement estimate from local contractors.

Coverage to Insure Your Home’s Structure

The core of homeowners insurance coverage is dwelling protection.

Dwelling Coverage

Dwelling Coverage covers the physical structure of the home, including walls, roofing, flooring, built-in appliances and attached structures. The right dwelling cover should be the same as the total amount it would cost to rebuild the dwelling, not the amount the dwelling is worth on the market.

Factors to Consider for Dwelling Coverage

Dwelling coverage calculations are influenced by a number of factors including construction materials, square footage, roofing type, custom features, labor costs and local permit requirements.

Plaster walls, handmade architectural features, hardwood trim are all common architectural elements in older homes that tend to cost more to replace.

Guarding Against Rising Costs

Building costs can escalate quickly because of inflation and a lack of workers. Dwelling limits are automatically adjusted up for inflation each year under the Inflation Protection endorsement.

Extended Replacement Cost coverage will pay more than the stated limits in the event of a regional disaster where the costs of the rebuild exceed the policy estimate.

Other Structures Coverage

Other structures coverage provides coverage for detached garages, sheds, fences, gazebos and workshops. Most policies offer 10% of dwelling cover, although this might not be sufficient for larger detached buildings.

Is Your Home Up to Code?

Additional rebuilding costs due to changes of the building codes after the loss. When reconstructing an older home, you may need a new electrical wiring system, plumbing system, insulation or accessibility improvements. These additional compliance expenses are funded by ordinance/law endorsements.

If Your Home Is Older, Will You Need a Policy to Cover Hard-to-Replace Features?

Handcrafted woodwork, stained glass, slate roofing or plaster detailing are features common to historic homes that can significantly raise replacement costs. There may be insurance policies available that will help cover the replacement of difficult materials and construction methods.

| Additional Coverage | What It Protects Against |

|---|---|

| Flood Insurance | Flood and storm surge damage |

| Earthquake Coverage | Earth movement and structural damage |

| Sewer Backup Coverage | Drain and sewer overflow damage |

| Extended Replacement Cost | Construction cost increases after disasters |

| Scheduled Personal Property | Jewelry, art, collectibles, luxury items |

Coverage to Insure Your Stuff

Personal possessions have a large value in the total household wealth.

Personal Property Coverage

Its Coverage is for furniture, electronics, clothing, appliances, tools and household items. Most insurance companies use a 50% to 70% ratio to determine the value of personal property.

Actual Cash Value vs. Replacement Cost Coverage

Actual cash value coverage deducts depreciation from the payouts. Replacement Cost – covers the cost of replacing the same items, new items, and with no discounts for depreciation.

Replacement Cost gives more financial protection following losses.

Named Perils vs. Open Perils

Named Perils policies only apply to events listed. Open Perils policies exclude risks specifically mentioned in the contract, otherwise the policy covers a wider risk.

Open Perils coverage is typically more expensive and covers more than open perils.

Coverage for Valuable Items

Items such as jewelry, firearms, collectibles, watches, art and luxury electronics are commonly not covered for the standard limits.

The Schedule High Value Personal Items endorsements are for more extensive coverage and higher reimbursement amounts.

Protect Your Personal Finances

The liability protection helps to ensure that lawsuits do not put personal assets and future income at risk.

Personal Liability Coverage

Personal Liability Coverage provides coverage for injuries or accidental property damage claims and legal costs.

Homes where there is a pool, dogs, a trampoline, rental property, or activities such as lots of guests will have increased liability exposure.

Medical Payments Coverage

Medical payments coverage is designed to cover minor injuries to guests, without regard to who is at fault. Coverage maximums are typically less than liability coverage maximums.

Consider an Umbrella or Excess Liability Policy

The liability coverage for umbrella policies goes beyond the coverage provided by homeowners and auto insurance policies.

Wealthy families typically buy umbrella policies that provide $1 million to $5 million in extra coverage.

Additional Home Insurance Coverages You Might Need

In addition to the basic homeowners insurance, many homeowners need endorsements or additional coverage.

Extended Replacement Cost

Extended Replacement Cost coverage tops up on payout amounts over dwelling coverage in the event of a regional disaster and the cost of rebuilding increases.

Inflation Protection

As building costs and material prices change, so do the policy limits with Inflation Protection.

Earthquake, Hail, and Windstorm Coverage

Earthquake and windstorm endorsements cover risks that are covered under most policies.

Windstorm deductibles and storm endorsements are often required in coastal areas.

Flood Insurance

It will pay for storm surge and rising water damage. Flood insurance is not part of a standard home insurance policy.

Sewer Backup Coverage

Water backup endorsements safeguard against sewer backup and/or overflows that affect flooring, drywall and property.

Schedule High-Value Personal Items

Personal property endorsements are used to cover the value of valuable property that an individual owns, and they are usually scheduled by the insurance company.

When to Reassess Your Coverage

The coverage should be reviewed annually and following significant life changes.

Up to date coverage is important after:

- Major renovations

- Home additions

- Purchasing expensive jewelry

- Starting up a home business

- Installing solar panels

- Doing kitchen or bathroom renovations

- Increase in local cost of construction work

Some insurance industry groups’ report, ‘What Matters Now – 2026’, identified inflation and labour shortages as key contributors to underinsurance risks.

How to Save Money on Homeowners Insurance

Don’t compromise coverage for lower rates.

Shop Around

Shop around for insurance quotes from different companies once a year due to different insurance pricing. Insurance companies may have a Resource Center and Tips & Tools section with calculators for quotes and information on how to compare policies.

Raise Your Deductible

With higher deductibles, your monthly insurance payments will be lower, but your claim cost will be higher when you need it.

Ask About Discounts

There are many types of insurance that offer a discount for:

- The combination of car and house insurance.

- Bundled auto and home policies

- Smoke detectors

- New roofing systems

- Claims-free histories

Upgrade Your Home

Claims risks and premiums are reduced with roof replacement work and plumbing and electrical upgrades, along with storm resistant materials.

Build Your Credit

Many states use credit-based insurance scores for determining insurance premiums. Homeowners insurance premiums may also be lower due to high credit scores.

Frequently Asked Questions

Q1: What Is the Proper Amount of Home Insurance?

The proper amount of homeowners insurance equals the full rebuilding cost of the home plus sufficient personal property and liability protection.

Q2: What Is the Rule of Thumb for Homeowners Insurance Coverage?

Most insurers recommend dwelling coverage equal to 100% of rebuilding costs and personal property coverage equal to 50% to 70% of dwelling limits.

Q3: What Is the 80% Rule in Homeowners Insurance?

The 80% rule requires homeowners to insure the property for at least 80% of rebuilding value to receive full claim reimbursement.

Q4: How Much Is Homeowners Insurance?

Homeowners insurance premiums vary based on location, rebuilding costs, claims history, deductibles, and risk exposure.

Q5: What Is the Difference Between Home Warranty and Home Insurance?

Home Warranty plans cover appliance and system breakdowns from wear and tear. Homeowners insurance covers sudden accidental losses such as fire, theft, and storms.