Key Takeaways

- Shop around and look at quotes from a few different life insurance companies to get the best coverage, the lowest premiums and the best policy benefits.

- Check insurance policy exclusions, coverage caps, riders and premiums before purchasing life insurance online.

- Compare life insurance quotes safely on the Internet by using secure comparison websites and checking the insurance company’s credentials.

- Life insurance rates are influenced by the age, health status, job, smoking history and term of the life insurance policy.

- Financial strength ratings, claim settlement experiences and customer reviews are some of the ways to determine a reliable life insurance company.

Introduction

When people compare life insurance quotes online they will be able to assess the options for coverage, premiums and the credibility of the insurance company that is looking to sell them a policy.

Life insurance safeguards the finances of the beneficiaries after the policyholder’s death; there are various forms of life insurance, and each provides varying levels of coverage, flexibility and long term value.

This guide will show you how to compare life insurance quotes online securely, look at life insurance policy specifics, steer clear of concealed dangers, and select the best life insurance policy for your personal and family monetary security.

What are Medicare Advantage plans?

Medicare Advantage plans are private health insurance plans that are approved by Medicare. These are Medicare replacement plans that offer Medicare benefits. Medicare Advantage plans are known as Medicare Part C plans. Medicare Part A is for hospital services and Medicare Part B is for outpatient medical services, like seeing doctors, lab tests, preventive screenings, and appointments with specialists.

Most vision care, dental care, fitness benefits and hearing aids are not covered by original Medicare. Medicare Advantage plans package these services together in one plan. Prescription coverage (Medicare Part D) is offered as part of most Medicare Advantage plans.

Some plans offer an annual out-of-pocket maximum, which caps the amount of money you’ll spend on health care within a single year. Unlike annual spending protection, this type of protection is not included in Original Medicare.

Medicare Advantage plans are run by private insurers and are subject to federal Medicare requirements. Even if a person chooses a Medicare Advantage plan, he or she will still be a Medicare beneficiary.

Definition and Overview

Medicare Advantage plan is an alternative option to get the benefits of Medicare from a private carrier. Medicare will reimburse insurance companies for administering care to people who sign up for them.

Because Medicare Advantage plans are not Original Medicare, the structure of these plans varies from Original Medicare in several ways, including that insurers build provider networks, determine copay amounts, and control prescription drug formularies.

The specifics of the plans vary from ZIP code to ZIP code and county to county. One reason why many seniors select Medicare Advantage plans is that having bundled coverage makes it easier to handle healthcare. Instead of having to join a separate health care plan, prescription plan, and other insurance plan, beneficiaries have coverage coordinated from one insurance provider.

Types of Medicare Advantage Plans

The Four Common Plan Configurations

Health Maintenance Org

Requires primary care doctor referrals to see a specialist. Strictly in-network except for true emergencies, but features lower copays.

Preferred Provider Org

Freedom to use out-of-network doctors without referrals, though in-network care is cheaper. Great for travelers and snowbirds.

Private Fee-For-Service

The plan determines exactly how much it pays providers. You can visit any doctor who explicitly accepts the plan’s unique terms.

Special Needs Plans

Highly customized coverage restricted to individuals with chronic illnesses (like severe diabetes or heart failure) or dual Medicaid eligibility.

There are multiple Medicare Advantage plan options. HMO plans, PPO plans, PFFS plans, and Special Needs Plans (SNPs) are the most common types of plans. HMO plans have strict provider requirements to be used, unless an emergency occurs.

Typically, HMO plans will require a referral before visiting a specialist. Usually these plans also have lower premiums and lower out-of-pocket expenses. Preferred Provider Organization (PPO) plans offer greater choice in providers. PPO members may visit doctors outside of the network, but care received from doctors outside the network is more expensive.

PPO plans are well-liked amongst retirees who travel frequently or spend time in a number of states. Private Fee-for-Service (PFFS) plans are plans that let members use a provider that agrees to accept the PFFS plan’s terms and conditions. Medical Savings Account (MSA) plans are a mix of high deductible plan insurance and health savings account.

Special Needs Plans are designed for individuals who are eligible for Medicare and have chronic diseases, or institutional care needs and/or Medicaid eligibility. SNP’s manage care for complex conditions like diabetes, heart disease and kidney disease.

How Medicare Advantage Works

Medicare Advantage plans make agreements with healthcare providers to establish provider networks. Plan rules determine who beneficiaries can choose to see as their doctor or facility in those plans. The Plan reimburses providers for covered services based on negotiated rates.

Premiums, copays, deductibles, and prescription expenses are paid according to the plan design/structure. Most plans will cover preventive care services, like annual wellness visits, screenings, vaccines, and chronic disease management programs. Emergency care is covered nationwide and won’t be limited by the network.

Comparing Medicare Advantage with Original Medicare

Medicare and Medicare Advantage plans vary in the providers available, cost, additional benefits, and prescription coverage.

Beneficiaries can go to almost any Medicare service provider in the country that accepts Medicare. Provider Networks are different with Medicare Advantage plans, which can cause limitations in doctor access.

Original Medicare doesn’t have annual limits on out-of-pocket costs. Yearly maximum spending limits also limit the costs for seniors who spend a lot on their medical care.

Many Medicare Advantage plans offer additional coverage and benefits, including prescription coverage and services like dental care, hearing aids and fitness memberships. Typically, Original Medicare necessitates having both a Part D and Medigap plan to get equivalent coverage.

If you have to see a provider frequently, you might want to opt for Original Medicare since access to providers is better nationwide. Those seniors who are looking for more affordable rates and package deals may want to choose Medicare Advantage plans.

Why Choosing the Right Medicare Advantage Plan Matters

Retirement brings a large rise in health care expenses. Selecting the proper Medicare Advantage plan will aid manage long-lasting wellness costs and access to medical care. Having a plan that costs low monthly premiums could have a small network of providers or high copay for any specialist.

Another plan that may cost more may offer more generous provider coverage and lower prescription charges. When comparing healthcare costs, it’s not so much the monthly premiums that matter, it’s the total annual cost of healthcare.

An improper plan can bring about unexpected expenses, prescription coverage issues, referral delays or limited hospital access. An annual review enables beneficiaries to adjust the coverage as their healthcare requirements evolve.

Compare Medicare Advantage Plans Side by Side

When you compare plans side by side, you’ll be able to see the differences in coverage and healthcare costs. Beneficiaries should compare:

- Monthly premium amounts

- Deductible levels

- Annual out-of-pocket maximums

- Prescription drug formularies

- Provider networks

- Referral requirements

- Specialist copays

- Emergency care coverage

- Dental and vision benefits are available.

- Star ratings

A low premium plan might charge high drug copay. Premiums are likely to be higher for a plan that has a larger provider network. Side by Side comparison eliminates enrollment errors.

What to Consider in a Medicare Advantage Plan

There are a few key considerations to take into account when deciding if a Medicare Advantage plan meets healthcare needs and financial goals.

Coverage for Prescription

Prescription Check: Before You Sign Up

Drug formulas change annually. Use this checklist to verify your out-of-pocket exposure:

The cost of prescription drug coverage is an important component of total health care costs. The vast majority of Medicare Advantage plans contain Medicare Part D prescription advantages.

There will be variation in drug formularies among plans. Some insurance companies may categorize a drug in a low-cost tier and others may categorize the same drug as a specialty tier.

Beneficiaries should compare:

- Covered medications

- Preferred pharmacies

- Prior authorization requirements

- Quantity limits

- Monthly prescription copays

- Mail-order pharmacy benefits

Insurance plans that offer good coverage for prescription drugs are an important consideration for people who have chronic conditions.

Referral Requirements

Most HMO plans have preventative care physicians who need to refer you to a specialist for a treatment. Typically, PPO plans will cover direct access to specialists without a referral.

Rules of referral apply to individuals who need frequent specialist services such as those for cardiology, oncology, nephrology or orthopedic services.

Referrals that take longer than usual can disrupt treatment plans and cause patients with chronic conditions to become frustrated with their treatment.

Provider Networks

Provider networks decide which doctors and hospitals members pay the lowest price for using. Beneficiaries should check with the plan to make sure that their preferred providers participate in the plan network before they enroll.

Other networks may develop during the year that include hospital systems and/or physician groups.Hospital systems and/or physician groups may become part of networks throughout the year. Regularly updating provider directories each year helps to avoid access issues.

The provider networks are smaller in rural areas than in urban areas. Less access to providers could result in further distances for specialist care.

Out-of-Network Coverage

PPO plans have the flexibility to provide a member with access to providers that are not in the plan’s network, but with higher out-of-pocket expenses.

Most HMO plans will only permit non-emergency treatment by in-network providers.

Many retirees who travel regularly like PPO plans due to their flexibility when traveling for health care. Medicare Advantage plans provide emergency services across the country, without needing to meet network requirements.

Star Ratings

Plans are rated on a scale of one to five stars by Medicare. Generally, plans with a higher rating offer better health care quality, customer satisfaction and claims performance.

Star ratings measure:

- Customer complaints

- Preventive care performance

- Chronic disease management

- Customer service quality

- Drug safety management

- Appointment access

Star ratings enable beneficiaries to compare plans and determine which ones are more effective.

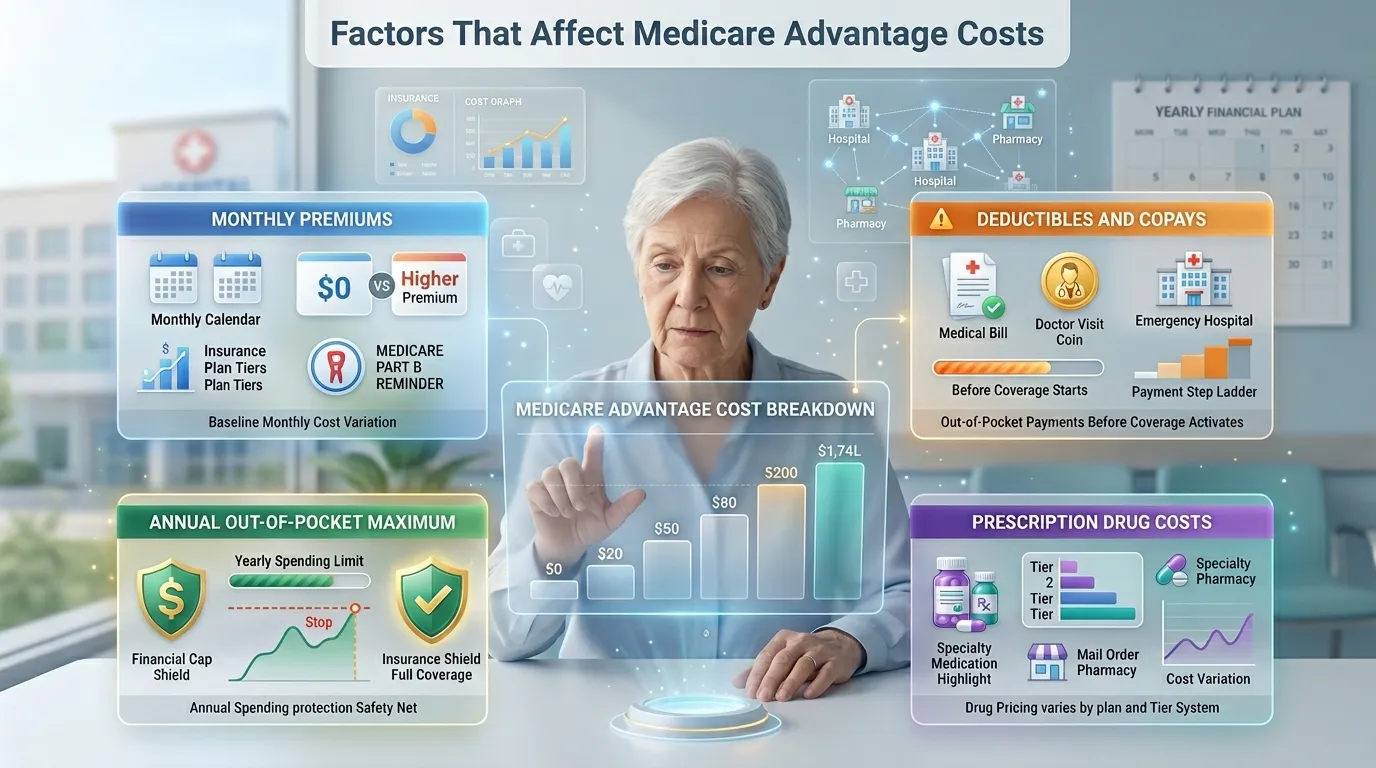

Factors That Affect Medicare Advantage Costs

There are a few factors that impact Medicare Advantage expenses.

Monthly Premiums

Some plans have a monthly premium of $0, while others have higher monthly premiums and more providers and benefits. Even if someone is enrolled in Medicare Advantage, they will have to pay the Medicare Part B premium.

Deductibles and Copays

Deductibles are the amount paid by the beneficiaries before coverage is provided. Copays will be charged for doctor visits, specialist visits, emergency services, hospital stays and prescriptions. Higher copays and deductibles are usually found in plans with lower premiums.

Annual Out-of-Pocket Maximums

Limits on spending every year will prevent beneficiaries from being charged an unlimited amount for health care. If the maximum is reached, the plan covers all health care costs for the rest of the year. Original Medicare doesn’t offer this coverage.

Prescription Drug Costs

The tier systems of drugs impact the cost of a prescription per month. Copays or coinsurance may be higher for specialty medications. Annual prescription coverage review is to avoid unexpected billings.

Tips for Choosing the Best Medicare Advantage Plan

The Golden Cost Rule

A $0 monthly premium plan can easily cost you thousands more over the year than a plan with a modest monthly fee. Look at your estimated Total Annual Healthcare Cost using this breakdown:

+ [Plan Medical Deductibles]

+ [Estimated Copays for Known Specialists]

+ [Your Expected Medication Tier Pricing]

= Your True Out-of-Pocket Liability

Seniors can make it easier to select a Medicare Advantage plan if they consider their priorities and not the hype.

Compare Total Costs

The monthly premium is not the only measure to look at when determining total healthcare costs. If you’re on a low-premium plan, but have high copays for specialist visits, you might end up paying more in the long run than if you were on a higher-premium plan and had lower copays.

Review Prescription Coverage Carefully

Medications are different each year. Beneficiaries should check to see that the prescriptions they are taking are still covered before renewing coverage.

Confirm Doctor Access

Participation of providers is subject to change. Making sure that providers are in network prior to enrollment can prevent unexpected change of doctors.

Check Extra Benefits

Some plans offer dental, vision, hearing, telehealth, transportation, and wellness benefits; these benefits are not covered by all plans. An analysis of the additional benefits is possible when comparing them.

Review Travel Needs

When it comes to traveler plans, it is preferable to have greater access to providers.

What to Look for in a Medicare Advantage Provider

Reputation of insurance company is important as you select Medicare Advantage plan.

Financial Stability

Well-capitalized insurers are likelier to operate efficiently on claims and have robust provider networks.

Customer Satisfaction

Insurers can be identified as being high in service quality by customer reviews and Medicare Star ratings.

Claims Support

Responsive claims support enhances healthcare experiences when billing disputes and authorizations are raised.

Plan Availability

Some insurers do not have coverage in all counties. The availability of a local plan is region dependent.

Red Flags to Watch Out For

Narrow networks and high cost-sharing requirements cause issues for Medicare beneficiaries with some Medicare Advantage plans.

Warning signs include:

- Few providers available; and

- High specialist copays

- Poor Star ratings

- Frequent customer complaints

- Expensive prescription tiers

- Complicated referral systems

Careful reading of plan documents will help to recognize any limitations early in the enrollment process.