Key Takeaways

- Renters insurance offers coverage of personal property, liability and temporary housing expenses resulting from a covered loss that occurs, such as fire, theft and vandalism.

- Typical renter’s insurance policies typically include Personal Property Coverage, Personal Liability Coverage, Medical Payments to Others and Loss of Use coverage.

- Common Exclusions on renters insurance policies are Flood Damage, Earthquake Damage, pest infestations and normal wear and tear.

- This policy is a more complete policy than the Actual Cash Value because the depreciation will not be deducted from the claim.

- Most renters do not think renters insurance is too expensive and can minimize economic loss due to disaster, lawsuit or burglary.

Introduction

Renters insurance is a policy that shields renters against financial damages to their personal property, liabilities and costs for temporary living expenses after a covered event.

The most common insurance coverage for renters include liability protection, property theft, fire damage, additional living expenses, water damage and mold coverage, and more.

This guide clarifies the scope of coverage under renters insurance, what is not covered, optional coverage options and how renters can select the best coverage for their apartment, condo, dorm and rental home.

How Does Renters Insurance Work?

| Coverage Type | What It Actually Pays For | Standard Limits |

|---|---|---|

| 🛋️ Personal Property | Furniture, electronics, clothing, and appliances damaged by fire, theft, or vandalism. | $20,000 – $50,000 |

| 🛡️ Personal Liability | Legal defense costs and settlements if a guest is injured or their property is damaged. | $100,000 – $300,000 |

| 🏨 Loss of Use (ALE) | Hotel stays, restaurant meals, and moving costs if a fire/smoke makes the home uninhabitable. | 30% of Property Limit |

| 🩺 Medical Payments | Minor guest medical bills for injuries on your rental premises, regardless of who is at fault. | $1,000 – $5,000 |

Renters insurance operates in a similar fashion to that of homeowners’ insurance, except that it covers the losses after a deductible is paid. Deductible is the amount the renter will be responsible for paying in order to get insurance benefits.

A renter that has a $5,000 theft amount and a $500 deductible typically would be paid about $3500 after the claim is approved. The policy will provide coverage under the terms and conditions and Coverage Limits as specified on the Declarations Page of the policy. Typically, claims start with the documentation of the loss, enrollment with the insurance company and submission of evidence of damage or theft.

Accompanied by pictures, receipts, police reports, serial numbers and inventory sheets. If a fire damages the building and the tenants need to be temporarily relocated to a hotel, the expenses for moving to a hotel, the cost of the hotel room, food and travel can be covered under Loss of Use coverage. It’s a different story with liability claims.

If the renter has been determined legally responsible for any injury or damage to the guest staying in the apartment, then Personal Liability Coverage can provide the renter with his or her legal costs, settlements and Medical Bills.

Do I Need Renters Insurance?

Yes. Renters insurance can be very useful to most renters because in the event of a large-loss event, it can be expensive to replace their possessions. A lot of tenants do not appreciate the worth of personal property. The replacement value of furniture, smartphone, computers, games consoles, television, kitchen appliances, clothing and jewelry is estimated to be $20,000 to $40,000.

Renters insurance is even more crucial for those that rent with pets, costly electronics, collectibles or savings that may be in jeopardy in case of liability lawsuit. One of the common misconceptions is that College Students assume they are covered by their parents’ homeowners’ insurance policy.

Limited off-campus coverage for dorm rooms may be available under some parents’ policies, but may not cover students that live off campus or in an apartment. Many military families rent out an insurance while moving or deployed to insure their Military Equipment, Uniforms, electronic devices and belongings.

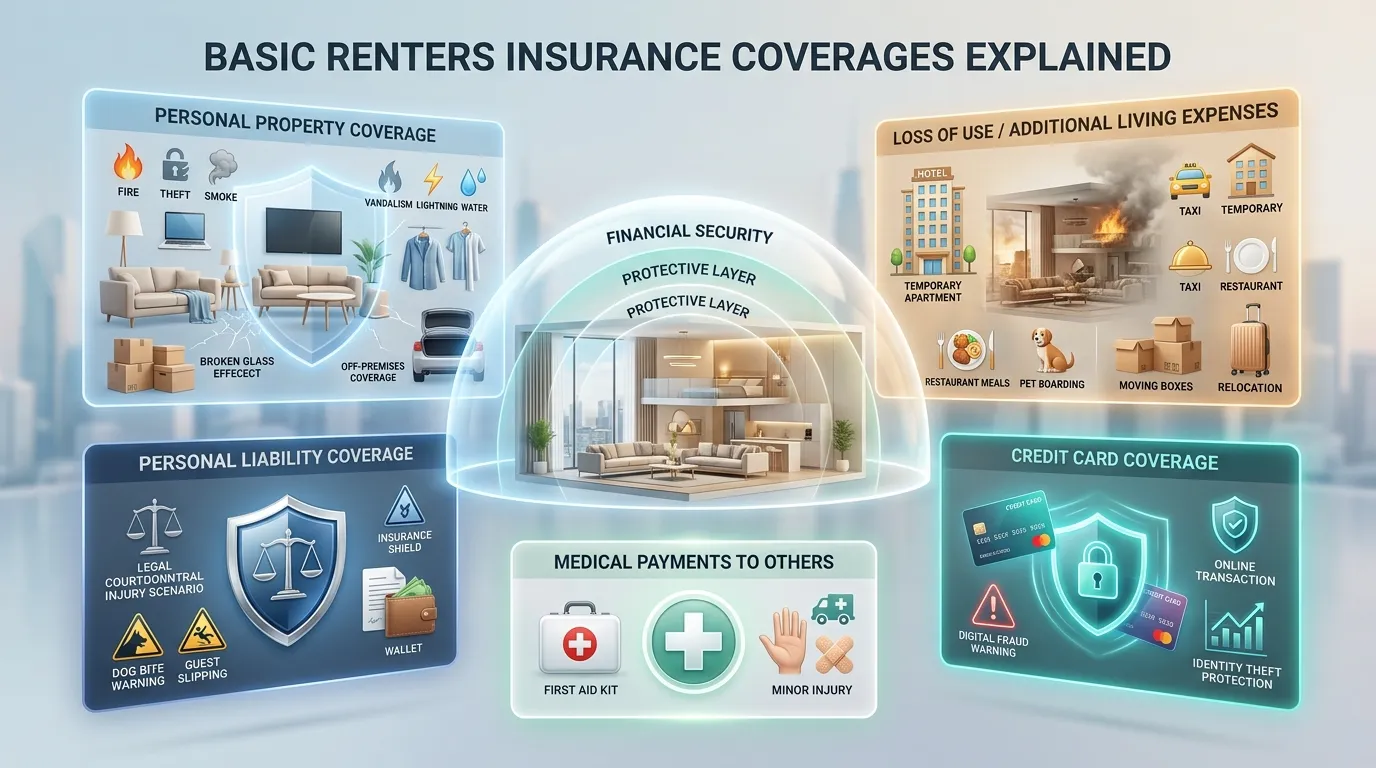

Basic Renters Insurance Coverages

Personal Property Coverage

Personal Property Coverage covers personal property following losses due to theft, fire, smoke, vandalism, lightning and some water damage. Coverage is provided for the contents inside the apartment and in certain instances coverage is extended to the exterior of the property.

These can include items that were stolen from cars, rooms and storage units, depending on policy. Most policies have Sub-limits on items like jewelry, firearms, watch, collectibles, cash, electronics etc. which have high valuations.

Scheduled Personal Property Coverage and/or Valuables Plus® endorsements may be needed for high value items. The advantage of Replacement Cost Coverage over Actual Cash Value coverage is that the value of the claims may be much lower due to depreciation.

Loss of Use / Additional Living Expenses

Loss of Use coverage will cover the Additional Living Expenses incurred by renters when they are unable to live in the apartment due to damage covered under the policy. Some of the expenses which may be included in TLE may include the cost of a hotel, apartment, restaurant meals, pet boarding, moving costs, and transportation.

If the tenant has a fire, heavy smoke or water damage, they will have to relocate for weeks or months until the damage is repaired. Loss of Use protection helps tenants to remain in their unit while it is safe and can be occupied.

Also, other insurers might cover the cost of temporarily moving the person insured after a fire to other apartments if the authorities don’t allow the insured to return to the building.

Personal Liability Coverage

Personal Liability Coverage is designed to help cover property damage and injury to tenants if they are being sued. The liability coverage will cover the cost of any settlements, legal fees and court costs if a guest enters the apartment, is injured by a pet bite, or is injured by a careless renter.

If you are renting, liability insurance is a huge factor to take into account, especially if you have a dog, access to a swimming pool, bicycles, a drone or regular guests. Usually, the liability coverage of a typical renters insurance policy falls between $100,000 and $500,000. Frequently, liability limits that are increased cost only marginally.

Medical Payments to Others

Medical Payments to Others covers for smaller medical bills when guests are injured on the property, even if it is not at fault. Coverage will provide for emergency treatment costs, hospital, ambulance, cost of minor injuries may be paid up front with no lawsuits filed. Medical payments coverage usually will have lower limits as compared to Personal Liability Coverage.

Building Additions & Alterations

Some tenants shell out their own money to enhance the light fixtures, cabinets, the floor, or other features of their apartments. The Building Additions & Alterations coverage covers tenant additions/alterations after covered losses.

It actually comes into play when you are renting a unit for an extended period of time and are making changes to it as your tenant.

Credit Card Coverage

Some renters insurance policies will cover stolen credit cards, forged checks or fraudulent transactions (limited Credit Card Coverage). In general, coverage limits are limited and coverage can be beneficial when you’ve suffered any financial losses from a theft.

Brand New Belongings®

Many insurance companies have a Brand New Belongings® program to cover replacement costs of damaged property in the event of a claim. Once the losses are covered, insurers could replace retired goods with new goods instead of with depreciated goods.

| Coverage Type | What It Covers | Why It Matters |

|---|---|---|

| Personal Property Coverage | Furniture, electronics, clothing, appliances | Helps replace belongings after covered losses |

| Personal Liability Coverage | Injuries and property damage claims | Protects against lawsuits and legal expenses |

| Loss of Use Coverage | Hotel stays and temporary housing | Pays living expenses if the apartment becomes uninhabitable |

| Medical Payments to Others | Minor guest injury expenses | Helps cover medical bills regardless of fault |

| Credit Card Coverage | Stolen credit cards and forgery | Provides limited financial reimbursement after theft |

Optional Renters Insurance Coverages

Replacement Cost Coverage

Replacement Cost Coverage is an insurance policy that provides coverage for the replacement of property without taking into consideration depreciation.

Actual Cash Value coverage reimburse in accordance with the age and usage of the item. With Actual Cash Value computations, a $1,000 television that is 5 years old may only be worth a few hundred dollars.

If your home is stolen or if a fire breaks out, Replacement Cost Coverage will provide you with greater financial coverage.

Scheduled Personal Property / Valuables Plus®

The Scheduled Personal Property Coverage will cover the value of high dollar items if the Policy has a limit of liability. Items that can be appraised separately include jewelry, luxury watches, cameras, collectibles, musical instruments and art. Valuables Plus® coverage can also cover items that are lost due to accident not theft or damage.

Water Backup Coverage

These usually aren’t covered by the standard renter’s insurance policy. Water Backup Coverage provides coverage against damaged systems due to backed up drains. When a water damage claim stems from an overflowing drain, it can ruin the flooring, electronics and furniture in a matter of weeks.

Theft Extension

Theft Extension provides enhanced coverage for stolen valuables and could expand off-premises theft coverage. Coverage may prove helpful for tenants with numerous appointments, or a lot of important belongings to store away from home.

Earthquake Coverage

Most renters’ insurance policies do not cover Earthquake Damage. Protection for earthquakes is offered in states where earthquakes are an issue, from endorsements or policies separately. Earthquake endorsements can include coverage for contents damaged by the quake, temporary housing and debris removal.

Pet Damage Liability

PDL covers damages caused by animals and injuries to animals to the renter/insured/owner. Every year there are numerous liability cases involving dog bites. Some insurers will have certain breeds that they exclude from their policies, others will have extra premiums for certain breeds.

Identity Theft Coverage

Identity Theft Coverage pays for costs related to identity theft fraud recovery, legal costs, lost wages and credit restoration services following an ID theft incident. Digital fraud continues to escalate and this is why a significant number of policies today offer protection for cyber-related issues.

Electronics Coverage

Electronics Coverage has more extensive coverage for your laptop, gaming system, camera, tablet and smart devices. The coverage may also cover accident damage, losses due to food spoilage after a power outage or electrical surge claims.

What Renters Insurance Does Not Cover

| Absolute Exclusion | Why It is Rejected | How to Secure Protection |

|---|---|---|

| 🌊 Flood Damage | Standard policies exclude rising surface waters, storm surges, or overflowing bodies of water. | Purchase separate policy through private carriers or FEMA (NFIP). |

| 🌋 Earthquake Damage | Earth movement and tremors are excluded across all base rental plans. | Add an independent Earthquake endorsement onto your base policy. |

| 🐜 Pest Infestations | Bedbugs, mice, and termites are categorized as long-term property maintenance issues. | Not insurable. Landlord is usually liable unless tenant lease rules state otherwise. |

| 👥 Roommate Belongings | Coverage is unique to the named individual. Unnamed roommates have $0 protection. | Require roommates to purchase an independent, individual policy. |

| 💼 Business Equipment | Work laptops, inventory, and professional camera gear face severe sub-limits ($2,500 max). | Attach a commercial home-business rider or separate inland marine policy. |

Flood Damage

A normal renter’s insurance plan will not protect against Flood Damage due to excessive water, storm surge or overflowing river. Flood Insurance must be purchased from the private insurance companies or government programs.

Earthquake Damage

Earthquake Damage is generally not covered by most renters insurance policies, and must be purchased as an endorsement.

Infestations (Termites, Pests)

Infestation by Termites, rodents, cockroaches and bed bugs and Pests are considered Maintenance related infestation and not as an Accidental Loss. Insurance companies usually refuse insurance claims that are related to infestation.

Roommate’s Belongings

When roommates are not mentioned on the same policy, Roommate’s belongings are typically not insured. Apartment renters insurance may afford a cleaner insurance coverage for communal living areas.

Appliance Malfunctions / Wear and Tear

Appliance Malfunctions is NOT caused by Normal Wear, Corrosion, Deterioration or Aging and is not covered. While insurance will cover for accidental damage that can happen anytime, it doesn’t cover gradual deterioration that may happen.

Items Used for Work (Business Property)

Typical renters insurance policies typically have limited business property coverage. Individuals who work from their home and have high-dollar equipment, photography items, stock or a home-based business might need extra endorsements to their business insurance.

Self-Storage Units (May Have Limited Coverage)

Depending on the wording of the policies, belongings within Self Storage Units can be afforded limited protection offsite. Storage unit coverage limits are generally significantly reduced as compared to coverage limits on premise.

Coverage Limits and Sub-Limits

What coverage limits are refers to the amount of coverage limits (how much will be reimbursed after covered losses). Sub-limits for items such as jewelry, fire arms, cash, silverware, collectibles and electronics.

For example, it may have an insurance policy that provides a $30,000 limit for Personal Property Coverage, but has a “high” limit for jewelry of only $1,500 unless that jewelry is covered by a separate policy. It’s crucial for renters to know the policy limits before they purchase coverage.

Actual Cash Value vs. Replacement Cost

If you are covered under an “Actual Cash Value (ACV)” policy, then the claim payment will be adjusted for depreciation. The older the item is, the less that will be paid because the insurance company will determine payout based on the current used value, not replacement value.

Replacement Cost is used to determine the cost of replacing the same items at today’s value, but without any depreciation. For most insurance professionals, Replacement Cost Coverage is a preferred option, as replacement costs following big losses can be overwhelming.

How Much Renters Insurance Do I Need?

The coverage amount for renter’s insurance depends on a person’s possessions, liability requirements and financial risk-tolerance level, and the location of their apartment. Prior to choosing coverage amounts, most renters will want to do a home inventory.

The cost of furniture, clothes, electronics, jewelry, kitchen ware and appliances can actually outpace expectations. Personal Property Coverage for many renters is between $20,000 – $50,000, and for high income renters, it’s a lot more! Our opinion is that liability coverage limits of $300,000 or more will provide you with more financial protection than coverage limits less than $300,000.

How Much Does Renters Insurance Cost?

Renters insurance is still one of the most affordable insurance policies offered. The amount of renters pay is based on their geographic location, deductible, apartment size, claims history and coverage and ranges from $10 to $30 per month.

If you have other policies then they can be combined with Auto Insurance policies and provide additional savings. Discounts are available from many companies such as GEICO, Liberty Mutual and Lemonade and can save a lot of money when purchasing Car and Renters Insurance Bundle.

Factors That Affect Renters Insurance Pricing

There are a few factors that affect renter’s insurance costs. The premiums are very sensitive to location. The location of the apartment can directly impact its insurance rates, and a location in a high crime area, or near an area that may be vulnerable to hurricane, wildfire or vandalism, will likely have higher insurance costs.

This will depend on coverage and deductible levels. The greater the deductible is, the lower the monthly premium will be, and the greater the deductible will be, the more it will cost the claimant.

Claims statistics, pet possession, credit-based insurance scores, apartment security systems and building age also have an impact on pricing.

| Optional Coverage | What It Protects |

|---|---|

| Replacement Cost Coverage | Replaces belongings without depreciation |

| Water Backup Coverage | Covers sewer and drain backup damage |

| Identity Theft Coverage | Helps pay fraud recovery expenses |

| Scheduled Personal Property Coverage | Protects jewelry, collectibles, and valuables |

| Pet Damage Liability | Covers liability involving pet-related injuries or damage |

Why Buy Renters Insurance?

Protection for Personal Belongings

Renters insurance also protects personal items in case of a covered event that results in water damage, fire or burns, theft or vandalism. Without insurance to replace the contents of your home, you can be in a lot of trouble.

Liability Coverage

The Liability Coverage applies to any damage or injury (not intended) suffered by the renter. In one serious lawsuit, years of saved money and future income is lost.

Additional Living Expenses

Additional Living Expenses coverage helps with the resiliency of renters’ housing after disasters. Without insurance, temporary relocation following fire losses can be very costly.

Peace of Mind

If there is an unexpected loss, renters insurance will help ease the financial anxiety. Coverage provides rentalers with a much quicker recovery from disasters, thefts or liability claims.

Landlord Requirements

Nowadays, many landlords are asking tenants to have renters insurance prior to the leasing of an apartment or home. Landlords will want tenants to have a liability coverage, or else they may end up facing litigation, and damage to the property. Proof of insurance may be required prior to the move in dates.

Renters Insurance vs. Landlord’s Insurance

Landlord’s Insurance is for the landlord’s building structure, common areas and landlord’s property. Renters Insurance will provide coverage for the tenant’s property, liability and temporary living expenses. Tenant’s furnishings, clothing, electronic equipment and liability problems are not covered by landlord insurance.

Special Situations

College Students

For college students that live in a dormitory, there may be some coverage provided under their parents’ policies; however, for those living off campus, renters insurance may be necessary.

Roommates

Establish if they are a multi-tenant or if individual policies are needed.

Subletting

Occupancy data is important to insurers and may necessitate policy changes when there are subletting situations.

Moving to a New Apartment (Transferring Policy)

Renters insurance can easily be moved to a new apartment by notifying the insurance company of the move.

Military Equipment

It may be necessary to have coverage for certain items on military uniform, tactical equipment or risks relating to military deployment.

Coverage Under Parents’ Policy

Sometimes, young adults also are covered partially on their parents’ homeowners policies when they are attending college full-time. Restrictions can still be in place for off-campus housing.

Summary