Key Takeaways

- Compare Rates Annually: The No. 1 best way to get competitive market rates is to shop around and compare quotes from various national and regional insurers at least once a year.

- Optimize Deductibles Strategically: Higher deductibles on both physical damage coverages (deductibles on comprehensive and collision coverage) can reduce your premium costs for physical damage coverage by 15-30%.

- Leverage the Power of Bundling: If you bundle auto insurance with a home, renter’s or condo policy with the same carrier, you can save up to 25% on both policies.

- Maintain Behavior Metrics: Drive responsibly and improve credit-based insurance scores with a clean driving record and these will fall into lower risk tier categories which will trigger automatic insurance rate reductions.

- Utilize Telematics and Rewards: Usage-based insurance (UBI) and pay per mile programs measure real driving to give up to 40% discount for low mileage and good driving.

Introduction

This is an effective way of doing more with your personal finances and less with your monthly expenses if you’re looking to save money this year on your car insurance. Knowing the factors insurance underwriters consider when determining risk can help you adjust coverage amounts, deductibles, or policy types to maximize your benefit.

With these targeted changes to your policy, you can still enjoy the same protection level, and save a lot of money each year.

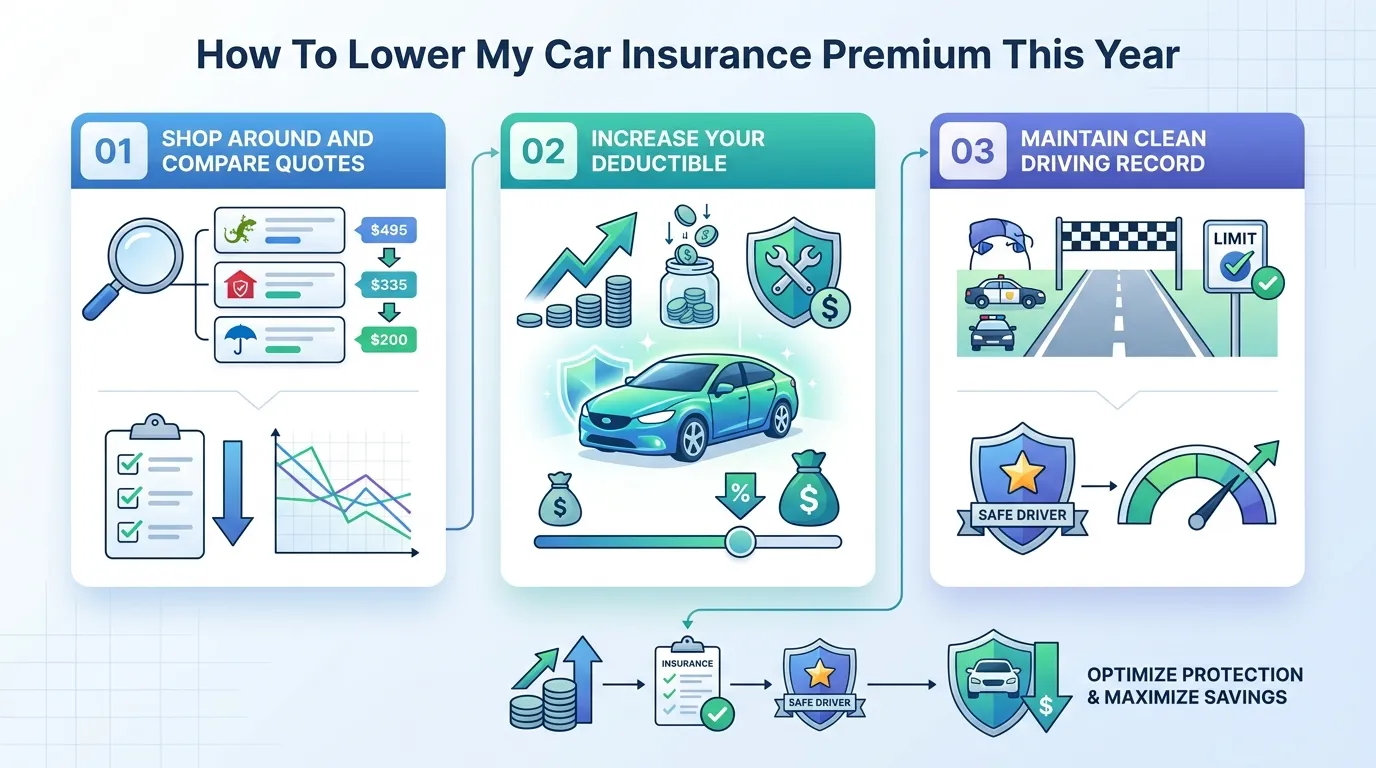

Shop Around and Compare Quotes

Driving around once at least once a year is the best way to reduce car insurance rates. The pricing model and risk appetite of insurance companies can vary often, so the best deal from last year may not be available this year. Get at least three quotes from national carriers and two regional insurers to get a baseline idea of market rates.

To make sure you can make an apples-to-apples comparison of the rates you’re offered, be sure to ask the same coverage limits, liability caps and deductible amounts for each comparison. Get rates from big name insurance companies like GEICO, Progressive, State Farm, Allstate, and Liberty Mutual.

If you’re looking to compare insurance companies, you should check out local insurance providers in your area, such as Mercury Insurance in California and Texas. Don’t wait till the end of your current policy before shopping around.

Most insurance companies will let you change coverage mid-cycle, and will give you a prorated refund of your unused premium. If you contact a competitor, make it clear that you are asking your current carrier for a loyalty retention offer to determine whether they will be able to provide a similar lower rate.

Increase Your Deductible

The out-of-pocket amount a policyholder must pay before the insurance company pays a physical damage claim is known as the insurance deductible. The underwriters are inversely related to deductibles: higher deductibles are directly associated with lower premium rates. You will be taking on more of the upfront repair expenses, which reduces the liability of the insurance company.

The best way to reduce insurance costs without compromising safety is to raise the deductible in a smart manner, depending on your savings liquid buffer. With a collision and comprehensive carrier deductible of $500, you might save 15% to 30% on your collision and comprehensive rates from switching to a $250 deductible to a $500 or $1,000 deductible.

Changing from a $250 deductible to a $500 or $1,000 deductible may save you 15% to 30% on collision and comprehensive rates. In the event that you choose to have a higher deductible ($1,000), put that amount of money into a savings account that you only use in an emergency situation to cover your deductible.

Maintain a Clean Driving Record

A clean driving record is definitely the most important factor in obtaining affordable auto insurance quotes because insurance companies rely on their past record of behavior to determine risk. When drivers get tickets for speeding, reckless driving or are cited for an accident where they were definitely responsible, it indicates a high-risk profile to underwriters and, consequently, premium inflation for three to five years.

Accident free driving equals lower risk levels for insurance companies. Don’t break the law by driving over the speed limit or by driving distracted. If you do get a traffic ticket, you can ask the local court whether it’s possible to take a traffic safety course or an approved defensive driving class to avoid having the ticket on your public motor vehicle record (MVR). One car accident caused by a person can raise auto insurance costs by 20% to 42%, and three years of driving with no at-fault accidents usually leads to automatic at-fault discounts.

Improve Your Credit Score

A specialized credit-based insurance score is used by insurance companies in the vast majority of states in the U.S. to predict the chance that a policyholder will file a claim. The statistics from the actuarial analysis of insurance claims revealed by insurance companies demonstrate that there is a clear statistical relationship between a higher credit score and a lower number of insurance claims.

Thus, individuals who have a good credit history will pay cheaper auto insurance than those who have bad credit. Keep an eye on your credit report to look for and correct any inaccuracies and take advantage of a credit score bump to qualify for reduced premiums. Clear away balances on revolving credit accounts so as to have less than 30% credit utilization ratio.

To build a track record of financial reliability, always pay your credit cards, auto loans and utility bills on time. Insurers in certain states, such as California, Hawaii and Massachusetts, are not allowed to use credit scores to determine premiums. In states like Texas or any other state where it is legal, though, if your credit can be improved, insurance can be reduced by up to 20%.

Take Advantage of Discounts

Available Structural Discounts Directory

There are various types of discounts insurers provide to make sure that they get customers who have a less high risk profile and keep the customers they already have. Get an itemized inventory of all household discounts from your current agent so you can be sure you’re not overlooking structural discounts.

Multi-Policy and Bundling Discounts

People who buy more than one policy from a single insurance company receive multi-policy discounts and bundling discounts. If an individual purchases auto and home, renters or condo insurance from the same insurance company, the premium for both policies is lowered. This bundling allows you to streamline your household bills and reduce the amount of premiums you pay for all your automobiles by 10-25%.

Multi-Car Discounts

If you have two or more vehicles covered by one policy, you will be eligible for multi-car discount. Multi-vehicle discounts are available from insurers because they can save on administrative cost by having one account for multiple vehicles. The vehicles covered under the policy should be at the same address and used mainly by household members to secure premium discounts of up to 25% on the liability sections of the policy.

Good Driver Discounts

Good driver discounts are offered to drivers who roll off the books without any accidents, moving violations or claims over a three to five-year period. These safe driving rewards can save you 10% to 30% off of your carrier based rate. The discount automatically applies after the insurer’s accident-free period of time.

Good Student Discounts

Young driving has a high rate of initial insurance premiums because they are inexperienced, as revealed by statistics. Students, however, who are currently enrolled in high school or a college course can get good student discounts by excelling academically from ages 16 to 24.

Save 10% to 25% on your auto insurance by providing your insurance provider with a recent report card or transcript with an average grade of B or a cumulative Grade Point Average (GPA) of 3.0.

Safety and Anti-Theft Discounts

A vehicle with an advanced safety system and an approved anti-theft system is less expensive to insure since it helps reduce injuries and makes it more difficult to steal. Vehicles with factory-installed ABS, electronic stability control, passive restraints, or factory-installed GPS anti-theft tracker have premium reductions.

Low Mileage Discounts

Low mileage discounts are available if you drive fewer miles than the national average (about 13,500 miles or 21,726 km annually). Anyone who drives in a short commute or someone that takes advantage of public transportation may not pose as much risk to the insurance company since they spend less time on the public road.

Let your insurance company know if you are driving less than a specified number of miles a year, such as under 7,500 miles per year (12,070 km per year).

Group Insurance Discounts

Insurers are in the business of forming partnerships with certain organizations that provide discounts for group insurance for their members. Ask your employer, university alumni association, labor union or military branch if they have an affiliation with insurance companies. This kind of discount is available for groups of 10 or more people and can save you 5-15% on your base premium.

Defensive Driving Course Discounts

Enrolling in a defensive driving and accident prevention course is a sign of learning safe driving skills. Some states have policies that incentivize insurers to provide defensive driving course discounts to those who complete a certified course.

The savings kick in more strongly for mature motorists (age 55+) and young motorists (age 25-).The savings are more pronounced for mature motorists (age 55+) and young motorists (age 25-), resulting in discounts of up to 5 percent for up to three years.

Usage-Based Insurance Discounts

By signing up for a Usage Based Insurance (UBI) program your insurance provider can monitor your actual driving behavior on the road. USI discounts are based on safe driving practices, including gradual braking, driving slowly, and driving less at night, and can be up to 10–40% off the base rate.

Consider Usage-Based Insurance (Pay-As-You-Drive)

| Tracked Habits | Safe Patterns (Discounts) | Risk Behaviors (Surcharges) |

|---|---|---|

| 🛑 Braking Pressure | Gradual Slowdowns | Hard Braking Events |

| ⚡ Acceleration | Smooth & Linear Starts | Rapid Speed Surges |

| ⏰ Time of Day | Standard Daytime Commutes | Midnight/High-Risk Hours |

| 📈 Speed Limits | Strict Adherence to Law | Excessive Velocity |

Pay-As-You-Drive (PAYD) insurance, also referred to as Usage Based Insurance, shifts the focus of insurance premiums from generalised information about you to information gained from your driving. You are monitored by insurers by fitting a plug-in telematics device into the car’s diagnostic port or through an app for your smartphone.

The Mercury Drive Safe Initiative or Progressive’s Snapshot uses programs to check driving habits under 4 key factors: deceleration patterns, acceleration rates, total mileage, and total hours driven.

These discounts can be very deep, performance-based, and in exchange for driving less during peak hours, avoiding sudden braking and smooth acceleration.

Choose a Vehicle with Lower Insurance Costs

Your car’s make and model have a significant impact on the cost of your car insurance. If you are buying an auto, both new or used, do some research to find out about the models which have lower insurance. Car insurance companies review the cars based on claims data obtained from organizations such as the Insurance Institute for Highway Safety-Highway Loss Data Institute (IIHS-HLDI).

Underwriters review history of past claims to determine, on average, the amount of damage, repair costs and theft rates for each vehicle model. Specialty parts, high repair and more expensive engines are just some of the reasons special interest cars—luxury and sports cars—are more expensive to insure.

Conversely, practical cars (mid-sized sedan, crossover, compact SUV) have excellent safety features and low parts, resulting in low cost coverage. When choosing an insurer, ask those with a special green vehicle discount to help offset the premium base pricing of electric vehicles and hybrids.

Review and Adjust Your Coverage

However, as your car gets older and your income changes, having the same policy coverage may mean that you’re paying for unnecessary coverages. Check your coverage annually when you renew the policy to make sure the coverage you have reflects the value of your car in today’s market.

Raise Your Deductible

If you already have low deductibles, speak with your agent about increasing these amounts. The higher deductibles for collision and comprehensive coverage, the lower your annual premium will be.The greater your collision and comprehensive deductible, the lower your annual premium will be.

Just make sure that this increase is in your budget and that you have sufficient cash reserves to pay the additional out-of-pocket expense in the event you have to make a physical damage claim.

Drop Unnecessary Coverage on Older Vehicles

Consider dropping optional physical damage coverage, such as collision and comprehensive coverage, for an older vehicle that has a low market value. The rule of thumb when it comes to financial considerations is if the annual cost of your collision and comprehensive coverage plus deductible is greater than the total actual cash value (ACV) of the vehicle, it may be a better decision.

Remove Optional Add-Ons

Review the details of your policy and cancel unused extras. Roadside assistance, towing and rental car reimbursement are just some of the extras which cost several dollars more on the premium each month. If you already have coverage for roadside assistance from a car manufacturer warranty or a credit card benefit, you should cancel the extra coverage that is included on the bill in order to reduce your expenses.

Bundle Home and Auto Insurance

One of the best ways to guarantee permanent premium discounts is to purchase a bundled policy. It is highly beneficial to insurance companies having multiple customers who use their services as it helps them retain more customers and reduces their administrative cost for marketing.

If you include your home, condo or renter’s insurance policies with your auto policy, carriers automatically apply a multi-policy discount to both lines.

Some insurance companies also have a ‘one deductible advantage’ that means if you have a claim such as a major storm that damages your house and your car, you only pay one deductible to settle your claim.

Install Anti-Theft Devices

Theft and vandalism are additional comprehensive claims risks of vehicles which do not feature modern security equipment. You reduce your risk profile, and get a special anti-theft device discount from your carrier, by taking proactive steps towards securing your vehicle. Contact your insurance company to obtain a list of anti-theft tracking systems and recovery devices that are approved.

The comprehensive part of your auto premium can be reduced by fitting an active GPS vehicle tracker, an electronic engine immobilizer or a steering wheel lock. ex=”0″ role=”button”>Others may mandate that insurers provide a discount for certain safety equipment, such as winter tires in cold-weather regions or steering locks in areas with high rates of vehicle theft.

Make Annual Payments Instead of Monthly

| Payment Cycle | Processing Costs & Surcharges | Bottom Line Financial Impact |

|---|---|---|

| 🗓️ Monthly Billing | Carriers impose recurring processing/installment fees ($2 to $7 per check) and occasional interest rates. | Adds up to $60+ extra per policy year |

| 💰 Lump-Sum Annual | Eliminates single transaction billing infrastructure, transaction overhead, and collection lapses. | Waives installment fees + up to 5% flat discount |

The way you pay your insurance premiums can increase or decrease your premiums over the course of your policy. Most insurance companies calculate policies in monthly increments to make them more manageable to pay, but this can also add an administrative expense.

With monthly payments, insurance companies charge installment fees (typically $2 to $7 per payment) for processing. Numerous carriers also charge an interest rate on financed premiums. Instead of monthly payments, consider paying these fees twice a year or once a year to avoid them.

If you pay a full six- or twelve-months premium, you’ll save on installment fees and may be eligible for a discount up to 5% off if you pay for the full policy.

Avoid Coverage Lapses

An insurance coverage lapse happens when an auto insurance policy is ended because of non-payments, cancellation or because of a delay in switching insurance companies, meaning that a person is without coverage for a short duration. It is important to prevent a coverage gap to ensure that long-term insurance costs do not rise.

Drivers who do not have insurance coverage continuously throughout have been considered high-risk drivers by the insurance companies. If you lapse the policy, underwriters assume that you were driving without insurance and can make you end up in a higher risk category when you reapply for a policy.

If you wait just a few days, your future premiums could rise by 8% to 15% per year. Do not cancel your vehicle outright if you’re thinking of selling it and putting it away for a while. Rather, discuss the option with your agent to go with a non-owner car insurance policy to keep a continuous history at a lower cost.

Explore Payment Options

If all of your premium is due at once is a burden to your liquid cash flow, you can look at other payment options to your insurance provider that will lower the administrative burden on you. The vast majority of insurance firms have choices for payment that will either lower or eliminate processing charges. Make recurring payments (AutoPay) automatically deducted from your checking account through Electronic Funds Transfer (EFT) or a credit card.

Automatic payments are the better option for insurance companies because they help to minimize the chances of missed payments and late notices. Carriers get you to sign up with them for a flat discount on your account when you sign up on paper, and they usually waive the monthly installment fees in exchange.

Plus, get electronic delivery of all policy declarations, bills and legal updates to qualify for a discount on your bill that avoids paper.

Review Your Policy Annually

📋 Mandatory Annual Policy Audit Items

- Commute Distance Assessment: Audit whether a transition to a remote or hybrid work schedule has lowered your daily mileage targets.

- Primary Address Verification: Log updates immediately if relocating to a lower-risk ZIP code with reduced historic theft metrics.

- Driver Roster Modifications: Formally remove young or student operators from the main risk ledger who have permanently relocated away.

- Vehicle Designation Parameters: Transition secondary or seasonal household automobiles from standard “commute” tiers over to the more economical “pleasure” use setting.

Your life changes over time and your car insurance policy should reflect that. When looking at an auto insurance policy, it’s easy to overlook the fact that these policies can be changed for a little extra savings. Regularly audit your policy paperwork on an annual basis.

If you have a new remote-work schedule or other changes, review your annual mileage and determine if you are driving less. If you’ve recently relocated to a different neighborhood, be sure to inform your insurer, since a different ZIP code could cause your rate to drop, depending on the neighborhood’s theft and accident history.

Remove a teen driver from your policy (or make a change to their status) if they move away permanently to go to college or a new job to reduce your premium.

Understand Factors That Affect Your Premium

| Risk Category | Key Underlying Variables Evaluated | Impact Scope |

|---|---|---|

| 👤 Demographics | Age, marital status, gender, and overall years of licensed driving experience. | Base Risk Tier |

| 📍 Geographics | Garaging ZIP code, local population density, vehicle theft rates, and weather patterns. | Location Based |

| 🚦 Behavioral | History of moving violations, at-fault accidents, and credit-based insurance scores. | Up to 42% Variance |

| 🛣️ Usage Tiers | Total annual mileage, primary vehicle purpose (commute vs. pleasure), and travel times. | Low-Mileage Discount |

| 🚘 Vehicle Metrics | Structural repair costs, safety ratings, vehicle weight, and built-in security features. | Model Specific Rate |

Car insurance rates could take into account a variety of factors, ranging from personal details, geographically relevant data, and vehicle-specific information. Knowledge of how they work together will help you to make more informed decisions to keep you costs low.

Your garaging ZIP code is used by insurers to study local vehicle theft statistics, vandalism and the average weather damage. The type of vehicle you use and how much you drive to work also changes your risk profile.

By knowing how these factors impact on your risk score, you can control your costs – from keeping your driving record clean, to building your credit, to choosing the vehicle that naturally has the lowest insurance premiums.

My Opinion